‘Give Me The $12,000 Back:’ Expert Reveals the Real Reason You Never Want to Put Money Down on a Lease. It’s Not What You Think

"I’m not taking those chances."

Conventional wisdom says putting money down lowers auto payments, but one car sales expert is flipping that logic on its head—and his reasoning might save you thousands if disaster strikes.

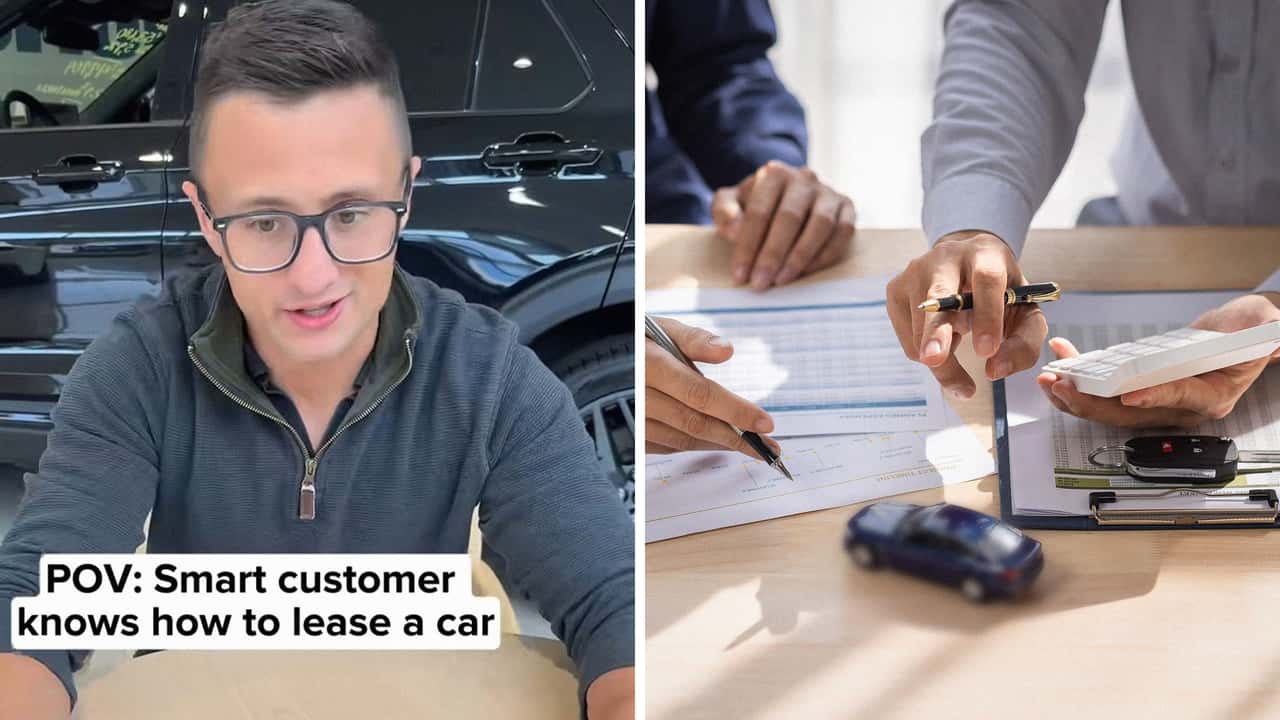

TikTok influencer Russell (@russflipswhips), who has amassed 789,400 followers and 39.5 million likes across more than 230 videos since February 2024, recently demonstrated why putting money down on a lease can be a costly mistake.

In a one-minute video showing a mock negotiation, he illustrates a scenario that every potential lessee should understand before signing on the dotted line.

The Setup

The video shows Russell at a hypothetical dealership desk with paperwork showing a $48,997 car lease, a $12,000 trade-in, and a proposed $499 monthly payment. But instead of accepting the standard deal structure, he makes a request that catches the salesman off guard.

“Look, man, I’ll lease the car, but I’m not going to put any money down with my trade-in. So can I just get that back in the form of a check?” Russell asks.

The confused salesman responds as most would, saying, “A check? What do you mean? Why don’t you just put money down? It’s going to make the payment higher.”

Russell then delivers the video’s key insight, “Well, here’s the reason I don’t want to put money down on a lease: it’s because what would happen if I total the car?”

When the salesman struggles to respond, Russell explains the harsh reality. “I’ll tell you what happens. If I total the car, they’re not going to give me any money back.”

Russell emphasizes the point, later adding, “If I put this money down and I were to total this car, I’m going to get absolutely zero back.”

A Smart Strategy

Trending Now

Instead of risking his $12,000 trade-in value, Russell proposes a safer approach. “So I’d like to do zero down on the lease,” the influencer says. “Give me the 12 grand back in the form of a check.”

He then flexes his insider knowledge, saying that the dealership’s insurance, “since it’s through Ford, it comes with included gap insurance, so I don’t need to put any money down.”

He’s willing to accept higher monthly payments in exchange for protecting his capital.

“I don’t care what the payment is,” he says, adding, “I’d just like to do zero down on the lease. Give me the $12,000 in the form of a check. I’ll do the first payment in plate fees, whatever that is, and I’ll just give you that out of pocket.”

Why This Works

The strategy hinges on understanding how gap insurance functions in leases versus purchases.

As Russell explains to the still-hesitant salesman, “It’s not smart to put money down on a lease. I’ll put a little bit of money down: Cash for the first payment and plate fees, but I’m not putting twelve grand down on the lease. I’m not taking those chances.”

Community Validation

The video resonated strongly with viewers who understood the financial wisdom behind the advice. User biglincoln79 commented, “Never ever put money down on a lease. Smart advice Russ.”

Another user, Rob Demmer, provided additional context. “At the end of the day, the total price of the lease paid over time is the same,” he said. “Definitely doesn’t make sense to put money down if you don’t need to!”

A user named Chris put forward a more nuanced view, writing, “Well, there’s a money factor in there so you’ll pay just a tad more by not putting money down, buuuuutt the protection it provides is WELL worth the minimal difference.”

Some viewers shared cautionary tales that proved Russell’s point. Sara Marguerite.xo recounted a nightmare scenario. “I put 8k down on a brand new car. Parked it at the gym and someone hit it and ran,” she recalled. “It got totaled. didn’t even have it a week, wasn’t even registered yet. Never putting money down again.”

The Gap Insurance Factor

Several commenters highlighted an important detail about manufacturer lease programs.

v3982 noted, “I didn’t know that Ford came with free gap insurance if you lease good to know,” while Larry5.0 confirmed, “That’s with just about everyone, haven’t seen a brand that doesn’t.”

However, movingon provided a crucial clarification. “If the value is less, gap won’t cover your down payment,” they noted, reinforcing why avoiding down payments on leases makes financial sense.

The strategy becomes even more compelling for business owners.

User madeyahlook explained, “Leasing vehicles is the only real move if you own a business. Depreciating assets are covered by your taxes. And you get to write off licensing fees, interest, mileage, and you always have a new vehicle.”

The Bottom Line

Russell’s approach challenges conventional thinking about lease negotiations. While putting money down reduces monthly payments, it also increases financial risk without providing the protection benefits that come with vehicle ownership. With gap insurance typically included in manufacturer lease programs, the traditional justification for large down payments disappears.

The video’s caption asks, “Would you rather lease a car or purchase a car?” but perhaps the better question is: If you’re going to lease, why risk your hard-earned money when you don’t have to?"

Motor1 sent Russell an email at his business address to request comment. We'll update this if he responds.

Trending Now

RECOMMENDED FOR YOU

Toyota 4Runner Driver Doesn't Want To Pay $20 Subscription To Start Car. Then She Discovers Key Fob Trick: 'The Things You Learn'

What Every Nissan Brake Caliper Color Means

Man Goes To Mercedes Dealership With Navy Federal Check And $10,000. Then He Goes To Carvana: ‘They Wanted A Copy Of My Degree’

Genesis Says There's Room For A Smaller EV

Volkswagen Driver Says She Puts Diesel In At The Pump—And The Men Around Her Always Say The Same Thing: ‘Men Come Running'

The Volvo EX30 Is (Was?) A Swing And A Miss

Woman Flirts With Man At A Family Dollar. Then She Makes A Comment About His Toyota: ‘Don’t Ignore That Red Flag’